Blockchain's Evironmental Impact

Source: Alexander LamDate: 2020-01-22

This article will address one of the biggest critiques of blockchain, and specifically the Proof-of-Work consensus protocol that Bitcoin uses: its environmental impact. We will examine some of Bitcoin’s power consumption estimates and what is being done to improve the Bitcoin network’s energy efficiency.

A Bad Case of Overestimation

In 1998, Mark P. Mills (who is currently a senior fellow at the Manhattan Institute, faculty fellow at the McCormick School of Engineering at Northwestern University, and strategic partner at Cottonwood Venture Partners) published a study entitled “The Internet Begins With Coal” in which he tried to estimate the amount of electricity that the Internet was using in the United States. According to his study, “The estimated total amount of electricity required by the Internet is compared, at the bottom of the table to the nation’s total electricity for all purposes and to the total growth in U.S. electricity supply. The results show that the approximately 100 million boxes on the Internet consume 8% of the total U.S. electric supply.” He goes on to use his calculations on the rate of Internet power demand growth to extrapolate the consumption requirements for the next two decades. His study goes on to say, “Based on recent history, and not assuming any acceleration in the Internet’s utilization, the magic cross-over to 50% of all electric supply consumed by the Internet would occur around 2020.”

Fast forward 22 years after the study was published, and Mills’ envisioned future of the Internet has not come to pass. According to the Berkeley Lab Energy Technology Area, U.S. data centers such as Google or Amazon are projected to consume approximately 73 billion kWh in 2020, and the U.S. Energy Information Administration reports that the U.S. produced 4.17 trillion kWh in 2018. At approximately 1.75% of total energy production, the Internet is in no danger of monopolizing all electricity consumption. The moral of the story here is that not only can extrapolation of past data be risky, but newer technologies like the internet often start out as inefficient and gradually improve over time.

The Global Banking System

Before we dive into Bitcoin and its environmental impact however, let us take a step back and look at the big picture, which is that it takes a lot of energy to run a global banking system – even the traditional one we have right now. It is difficult to estimate the energy consumption of the global banking system, but one model that does a good job of it comes from Carlos Domingo, Founder and CEO of Securitize. Please note that due to a few updated estimations, some of my input assumptions differ from his original Hackernoon post with his model, footnoted here.

First let’s estimate the number of banks in the world. On the low end, we have estimates such as the one from banking and payments consultant Faisal Khan, CEO of Faisal Khan & Co., which assumes around 8,000 banks in the US and an average of 30 banks per country for the approximately 220 other countries for a total of around 14,600 banks. Another estimate comes from David Gyori, CEO of Banking Reports, which recommends using the Accuity Bankers Almanac as an estimate with their database of around 25,000 banks worldwide. However, Gyori also notes that this only refers to the number of banking licenses and does not include “quasi-banks” such as credit unions, savings cooperatives, and savings associations that he estimates total around 60,000. Furthermore, this number does not include the number of “shadow banks,” which are non-bank financial institutions that provide credit outside the scope of regulators (i.e. investment banks, mortgage lenders, money market funds, insurance companies, hedge funds, private equity funds, payday funds, etc.). Averaging these three estimates of 14600, 25000, and 60000, we get 33200, which we will round down to 30000 to be conservative.

Instead of estimating the entire amount of electricity that these banks use, we will just count three costs: server costs, branch costs, and ATM costs, although there are other costs such as heating and lighting for non-branch offices. In Domingo’s model, he uses an average of 100 servers per bank which needs to provide sufficient IT infrastructure to support the bank’s own employees, its enterprise resource planning software (to manage processes such as financial operations and human resources), and other functions that the bank requires. In an article from ZDNet, they estimate that “one server can use between 500 to 1,200 watts per hour.” Using an average of 850 watts per hour, our 30000 banks using a total of 3,000,000 servers are using 22,338,000,000,000 watts per hour per year, or approximately 22.34 TWh per year.

For estimating branch costs, we can first look at the World Bank’s data from 2018, which estimates 12.728 commercial bank branches per 100,000 adults on average worldwide and a total of approximately 5.63 billion adults worldwide. Combining these two figures, we get approximately 716,000 commercial bank branches worldwide. The electricity consumption per branch is very hard to estimate but we will use Domingo’s estimation of 10 kWh per branch, including an estimated of 10 light bulbs per branch, 2 air conditioning units on 20% of the time, 12 desktop computers running an average of 12 hours a day, 20 days a month throughout the year. Altogether, these assumptions give us around 62.7 TWh per year total for all commercial bank branches in the world.

Lastly are the ATM costs, which we will estimate by first looking again at the World Bank estimates which gives a figure of around 41.6 ATMs per 100,000 adults in the world. As stated above, the World Bank estimates there to be approximately 5.63 billion adults worldwide, which gives us around 2.34 million ATMs worldwide. Using an estimation from an article in PR Newswire, a typical ATM requires 135 kWh per month, which would be 1620 kWh per year per ATM. Multiplying that figure by the number of ATMs gives us a total energy consumption of 3,790,800,000 kWh of energy per year for all ATMs or around 3.79 TWh per year.

So in total, this model estimates a yearly energy consumption of around 88.83 TWh for the global banking system including most services like sending money internationally, and withdrawing or depositing cash from one’s account. To put that in perspective, the country of Sri Lanka consumed a total of 94.203 TWh of energy in 2018, according to BP’s 2019 Statistical Review of World Energy. Please note that this figure is not just electricity consumption, but includes all forms of energy consumption. For further perspective, the two largest energy consumers in the world, China and the U.S., consumed around 38071 and 26756 TWh respectively. While these larger figures may dwarf the global banking system’s energy consumption, 88.83 TWh is approximately the amount of energy needed to power 8,096,062 American homes for one year (using an estimated 10,972 kWh of annual consumption per U.S. residential utility customer), showing that depending on how you look at it, energy consumption can seem very big or very small.

The Digiconomist Model

Moving on to what are some of the current estimates of the Bitcoin network’s energy consumption, let us begin with one of the most widely cited estimations, from Digiconomist. Started in 2014 by PricewaterhouseCoopers consultant Alex de Vries, Digiconomist publishes what it calls the “Bitcoin Energy Consumption Index (BECI)” footnoted here. The BECI gives an estimated TWh per year of energy that the Bitcoin network uses, based on a few assumptions that will be discussed below. Digiconomist and the BECI have been featured on many well-known news outlets such as the BBC and The Economist, and has even been referenced by billionaire investors such as Stanley Druckenmiller. In a December 2017 interview with CNBC, Druckenmiller mentioned a comparison found on Digiconomist between U.S. homes and the Bitcoin network when he told the host that even though he does not own bitcoin, “What I do know is it takes the same amount of energy to do one bitcoin transaction that it takes to power nine homes in the U.S. By 2019, it’ll take up half the energy in the United States to run the bitcoin network.” At the time of the interview with Druckenmiller, the BECI showed around a 34-35 TWh annual energy consumption from the Bitcoin network.

Digiconomist has four main steps involved in determining Bitcoin’s energy consumption: 1) Calculate total mining revenues 2) Estimate what part is spent on electricity 3) Find out how much miners pay per kWh 4) Convert costs to consumption. For step 1, mining revenues can be found at Blockchain.com which totals the daily amount of block rewards and transaction fees paid to miners, footnoted here. For step 2, Digiconomist assumes that miners will spend 60% of their revenues on operational costs on average in equilibrium, or in other words, the point at which producing new mining machines is no longer profitable. For step 3, Digiconomist assumes miners spend USD $0.05 per kWh on operational costs. And finally for step 4, all three figures are combined to create an estimate of the amount of energy the Bitcoin network consumes.

The Marc Bevand Model

Another model for estimating Bitcoin’s energy usage was done in 2017-2018 by Marc Bevand, a former Google employee, and current researcher, entrepreneur, and angel investor, footnoted here. Bevand’s approach from that of Digiconomist by focusing on the mining hash rates and energy consumption of some of the most common models of mining machinery including those from Bitmain (Antminer), Bitfury, and Canaan.

Firstly however, Bevand takes data on total daily Bitcoin hash rate from Quandl, a commonly used data marketplace for financial, economic, and alternative data. He then organizes the period between 2014 and 2018 (since his blog where he details his model was most recently updated in 2018) into “phases”, (i.e. Dec 2014 to Feb 2015, Feb 2015 to Jun 2015, etc.) based on releases and discontinuances of mining machinery. He then reached out to the machine manufacturers to conduct market research, including the respective market shares of each company. Based on each company’s market share during different “phases” and each machine’s efficiency (measured in Joules per Gigahash), Bevand is able to estimate a lower bound, an upper bound, and a best guess of total network energy consumption by assuming the network is using the most efficient machines, least efficient machines, or a mix.

After getting an estimate of energy consumption, Bevand uses an electricity cost of USD $0.05 per kWh as well as data on Bitcoin’s daily price to calculate what each mining machine would generate in revenue and profit, assuming miners sell their Bitcoins the same day they mine them. It is interesting to note that this part of his analysis reveals two key findings: 1) 70% of lifetime profits were generated in the first 30% of the machine’s life (with 80% of lifetime profits in the first 50% of the machine’s life) and 2) Mining was quite profitable, for example, “A miner who had invested $418 into purchasing an [Antminer] S5 [on December 27th 2014] would have [on July 9th 2016], after 561 days, turned it into $1012.37, a 2.4x gain.” He follows up the second finding by taking into account Bitcoin’s price appreciation as a major factor in mining profitability as he states, “Another investor who on December 27th 2014 2014 bought $418 worth of bitcoins would be worth $863 on July 9th 2016, a 2.1x gain. An important reason why mining was profitable was simply that BTC gained value.”

The University of Cambridge’s Model

In July of last year, the University of Cambridge’s Judge School of Business Centre for Alternative Finance launched their “Cambridge Bitcoin Electricity Consumption Index (CBECI)” based on the same approach taken by Marc Bevand. The input parameters are similar, and includes the network hash rate (updated dynamically from Blockchain.info), miner revenues (updated dynamically from Blockchain.info), mining equipment efficiency (taken from over 60 different types of mining equipment compiled in an excel footnoted here), electricity cost (which the models assumes to be USD $0.05 per kWh although the interactive website allows visitors to change this price), and data center efficiency (measured in Power Usage Effectiveness (PUE) which is defined as Total Facility Power divided by IT Equipment Power and serves as a ratio of how much energy overhead there is going into a data center towards things like cooling and lighting). Like Bevand’s model, the CBECI calculates a lower bound, an upper bound, and a best guess of Bitcoin’s energy consumption, which is then annualized and applied to a 7-day moving average to account for short term hash rate movements.

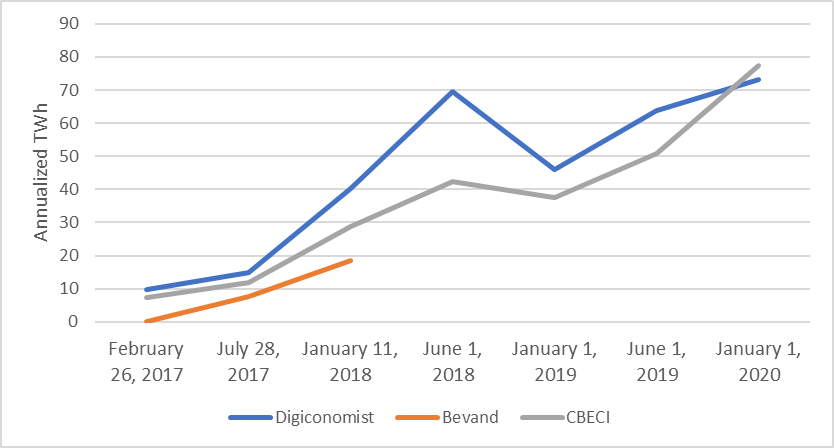

A Comparison of the Models

Below is data taken from all three models to show a comparison of Bitcoin network energy consumption estimates over time using the best estimates of each model (i.e. not the lower or upper bounds). Please note that the first three data points are selected due to those being the day where Bevand switches from one phase to another. Bevand’s estimates on his website end after January 11, 2018, and thus onward data is not available (N/A). Also please note that in instances where Bevand uses a small range for his best estimate, I take the average of the two ends (i.e. a best estimate range of 4.12-4.73 is 4.425).

Not All Power Is Created Equal

An important factor in any conversation about energy consumption, whether about Bitcoin or not, is where the energy is coming from. Digital asset management firm CoinShares estimates that globally, 73% of the electricity used to power the Bitcoin network is renewable, using data they gathered from their own research, Morgan Stanley Research, the U.S. Energy Information Administration (EIA), and several other sources. The research further shows that 54% of electricity used to power the Bitcoin network comes from one province in China, Sichuan, known for their abundance of hydro-power, especially during the rainy season. According to the South China Morning Post, “during the rainy season, Sichuan’s electricity tariffs drop to as low as 2 US cents per kWh…much cheaper than the 11 US cents reported in Guangzhou and Beijing.” Besides Sichuan, CoinShares also notes that miners tend to concentrate around areas where hydropower is cheap and the climate is relatively cool such as Quebec and the Pacific Northwest. For example, Hydro Quebec, which is a state owned company focused on the production and distribution of hydropower, estimates that the province has an oversupply in electricity equivalent to 100 TWh over 10 years, and offers cryptocurrency miners a rate of USD $0.0394 per kWh.

To briefly go into why hydropower is such a popular choice for miners, we need to take a look at the features of a hydropower dam. In his Hackernoon post, Robert Sharratt, a former investment banker specializing in natural resources and power writes, “Electricity systems are quite complicated, mainly because electricity cannot be stored, except in small quantities. So, you have the concept of pools, grid operator dispatch functions, etc. Hydro power is mainly located in mountains, a long way from population centers. The transmission line losses often make it unfeasible to transport the electricity supply to where it is demanded; consequently, a lot of hydro power in underutilized. Miners are highly mobile; they can move to where the cheapest power is, in a way that hospitals, schools, etc. cannot.” Sharratt goes on to say, “A few local industry experts told me that they estimated that at least 200-225 TWh per year of surplus hydro power exists, just in Sichuan.” It is important to note that while hydropower generators produce clean energy, the construction of the dam including production of manufacturing materials, and impact on the environment does have negative consequences.

However, there are critics that would certainly disagree that Bitcoin is “going green.” In a report titled “Renewable Energy Will Not Solve Bitcoin’s Sustainability Problem” published March 2019, de Vries argues that “the energy costs not only aren’t offset by renewable energy, but there are also other environmental costs we don’t fully appreciate yet.” Using data gathered from a report by China Water Risk (CWR), a Hong Kong based nonprofit aimed at addressing what they call the “country’s water crisis”, de Vries sees several problems in thinking about Bitcoin mining as environmentally safe.

First, de Vries notes that mining is not the only cost associated with Bitcoin, and the network includes services such as Bitcoin ATMs, exchanges, wallets, and payment solution providers, all of which consume energy. Second, he cites the CWR data which find high seasonality in the hydropower producing regions of China. In Sichuan, the CWR says that “the average power generation capacity during the wet season is three times that of the dry season.” During periods where rain is scarce, the CWR says power providers often turn to coal to make up for lack of energy supply. Third, de Vries says that the waste generated by the disposal of obsolete mining equipment must be taken into account as well. His report models that “the annualized e-waste generation would amount to 10,948 metric tons.”

Proof of Work: A Work In Progress

The different models we have covered so far have focused on Bitcoin’s Proof of Work consensus protocol, but there are alternatives to it as well. Among them is Proof of Stake, which the second largest cryptocurrency by market cap, Ethereum, was originally scheduled to switch to in early 2020. As future articles will go more in depth on the different consensus protocols, for now it is only important to understand that some alternatives like Proof of Stake can use significantly less computing power than Proof of work and thus require less energy.

Furthermore, although Bitcoin does not have any plans to change from Proof of Work to Proof of Stake as well, significant work has been done on improving the efficiency of the network with proposals such as the Lightning Network. Again, the Lightning Network will be covered in depth in a future article, but for the purposes of this article, it is only important to understand that it may allow for faster transactions by reducing the number of transactions that need to be recorded on the main blockchain, improving scalability.

Key Takeaways

As we can see, trying to estimate the amount of energy consumption the Bitcoin network uses compared to the global banking system for transactions is a very tricky process with limited information. With little over ten years in age, Bitcoin is a technology that is far from mature – and like the internet, it takes time for the ecosystem to both apply cryptocurrency as a solution to problems outside the industry, as well as fix existing problems with the cryptocurrency itself. Understandably however, our climate is changing faster than ever before, and the need to innovate and solve sustainability problems with current technologies such as Bitcoin is rapidly increasing.

References

1、https://www.heartland.org/_template-assets/documents/publications/6858.pdf

2、https://www.heartland.org/_template-assets/documents/publications/6859.pdf

3、https://eta.lbl.gov/publications/united-states-data-center-energy

4、https://www.eia.gov/tools/faqs/faq.php?id=427&t=3

5、https://hackernoon.com/the-bitcoin-vs-visa-electricity-consumption-fallacy-8cf194987a50

6、https://www.quora.com/How-many-banks-are-there-in-the-world-1

7、https://www.linkedin.com/pulse/how-many-banks-globally-david-gyori/

8、https://www.linkedin.com/pulse/how-many-banks-globally-david-gyori/

9、https://www.investopedia.com/terms/s/shadow-banking-system.asp

10、https://data.worldbank.org/indicator/FB.CBK.BRCH.P5

11、https://data.worldbank.org/indicator/SP.POP.1564.TO

12、https://data.worldbank.org/indicator/SP.POP.65UP.TO

13、https://hackernoon.com/the-bitcoin-vs-visa-electricity-consumption-fallacy-8cf194987a50

14、https://data.worldbank.org/indicator/FB.ATM.TOTL.P5

15、https://www.prnewswire.com/news-releases/diebold-innovation-leads-to-worlds-greenest-most-power-efficient-atm-250600621.html

16、https://www.bp.com/content/dam/bp/business-sites/en/global/corporate/pdfs/energy-economics/statistical-review/bp-stats-review-2019-full-report.pdf

17、https://www.eia.gov/tools/faqs/faq.php?id=97&t=3

18、https://digiconomist.net/bitcoin-energy-consumption

19、https://www.bbc.com/news/technology-48853230

20、https://www.economist.com/the-economist-explains/2018/07/09/why-bitcoin-uses-so-much-energy

21、https://www.cnbc.com/2017/12/21/no-bitcoin-is-likely-not-going-to-consume-all-the-worlds-energy-in-2020.html

22、https://digiconomist.net/bitcoin-energy-consumption

23、https://www.blockchain.com/charts/miners-revenue

24、https://digiconomist.net/bitcoin-energy-consumption

25、https://digiconomist.net/bitcoin-energy-consumption

26、http://blog.zorinaq.com/bitcoin-electricity-consumption/

27、http://blog.zorinaq.com/bitcoin-electricity-consumption/

28、http://blog.zorinaq.com/bitcoin-electricity-consumption/

29、https://www.cambridgeindependent.co.uk/business/cambridge-bitcoin-electricity-consumption-index-launched-9076175/

30、http://sha256.cbeci.org

31、https://www.cbeci.org/methodology/

32、https://digiconomist.net/bitcoin-energy-consumption

33、http://blog.zorinaq.com/bitcoin-electricity-consumption/

34、https://www.cbeci.org/

35、https://thenextweb.com/hardfork/2019/12/11/bitcoin-cryptocurrency-mining-hash-rate-china-renewable-energy-blockchain/

36、https://thenextweb.com/hardfork/2019/12/11/bitcoin-cryptocurrency-mining-hash-rate-china-renewable-energy-blockchain/

37、https://www.scmp.com/business/banking-finance/article/3035665/cryptocurrency-miners-tap-sichuans-cheap-hydropower

38、https://www.reuters.com/article/us-canada-bitcoin-china/chinese-bitcoin-miners-eye-sites-in-energy-rich-canada-idUSKBN1F10BU

39、https://www.eia.gov/energyexplained/hydropower/hydropower-and-the-environment.php

40、https://breakermag.com/new-report-says-renewable-energy-will-not-solve-bitcoins-sustainability-problem/

41、https://breakermag.com/new-report-says-renewable-energy-will-not-solve-bitcoins-sustainability-problem/

42、https://breakermag.com/new-report-says-renewable-energy-will-not-solve-bitcoins-sustainability-problem/

43、https://cointelegraph.com/news/binance-research-ethereums-switch-to-staking-will-transform-industry